Cutting-edge technology backed by a team of financial experts. Our platform is a one-stop solution for anyone seeking instant and guaranteed lending options.

Average Response Time

0.05 Hour

Customer Rating

0 Star

Average Loan Completion*

0 Days

Approved Lenders

180+

Why Choose Us?

Speed

Instantly match with specialist lenders that are pre-qualified and ready to fund your plans.

Access

Our platform gives you access to over 200 bespoke lending options, tailored to your requirements

Value

Our smart-search software means you’re guaranteed the best rates in the market. Plus, we don’t charge a broker fee.

Support

Monitor your enquiry in real-time, while receiving specialist support from our expert team of advisers.

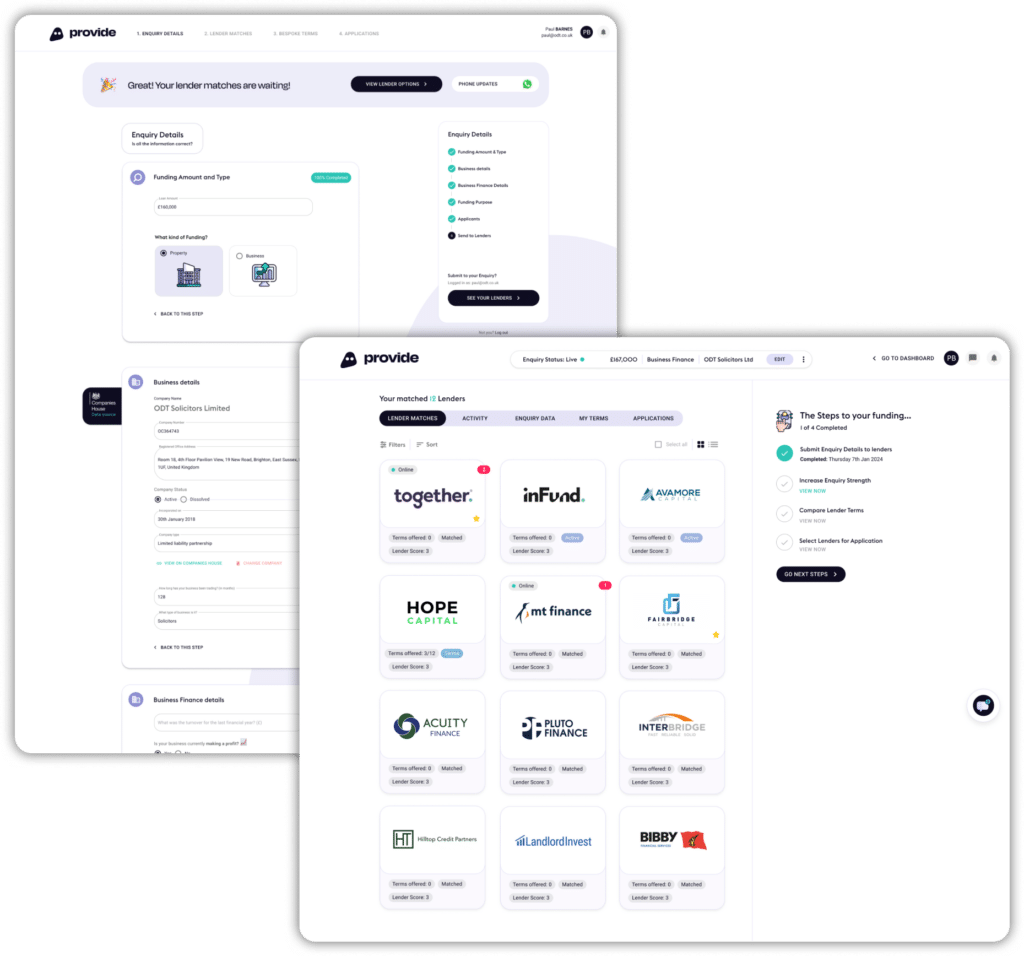

Provide Finance’s broker dashboard helps brokers deliver exceptional support to their clients. The platform incorporates software for brokers to quickly communicate and exchange secure documents with all parties, making the process as simple as possible.

I've been able to witness firsthand their unique combination of digital intuition and human touch to create a fantastic financing tool that has helped many of my customers.

Adam Tyler

Provide Finance provided exceptional service throughout the funding process, and Mihaela ensured that the transaction was completed with ease going above and beyond to ensure the deals were completed.

Neil PatelLondon Credit

A great completion with Provide Finance! Dealing with such a professional and knowledgeable team at Provide made the process with them a dream to work with and we our looking forward to working closely with them on the next deal.

Ian Miller-HawesBridge Invest

Fantastic experience working with Miranda and the Provide Finance team. Found some great rates for us and were supportive all through the process.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.